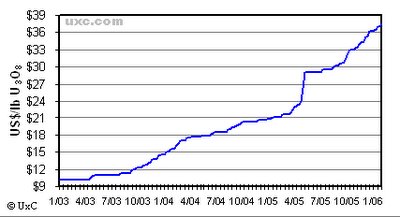

International Uranium Corporation (IUC.TO) One of the more intruiging uranium plays out there is a company with wide-ranging assets. This company is IUC, headquartered in Denver, Colorado and poised to capitalize on the growing interest in reviving uranium production in the United States

AssetsWhite Mesa MillThis mill is located in Southeastern Utah and is used to recycle waste material. While doing so, it can extract uranium and vanadium. In 2006, White Mesa is expected to extract half a million pounds of uranium, which IUC will sell at its own leisure. Vanadium, by the way, is used to reinforce steel among other things. Ferrovanadium, an alloy containing 50-80% vanadium, is selling at about $59/kg.

American Mines IUC owns two adjacement mines in Utah, Bullfrog and Tony M, which combine to form the Henry Mountains Complex. There are an estimated 24 million lbs of uranium oxide in these two mines, although they are not confirmed by industry NI 43-101 standards yet. IUC has stated that due to increased mining and milling costs that they would postpone the restart of production in Tony M until uranium prices were higher. IUC also own several mines in Colorado and Arizona, and does exploration there, although these do not be significant.

Canadian Exploration The jewel for IUC here is a 75% stake in Moore Lake, located 35 kilometres southeast of Cameco's McArthur River uranium mine, aka world's biggest uranium mine. Results posted on December 21, 2005 validated the existence of fairly concentrated uranium in Moore Lake: ML-100 returned 2% U3O8 over 7.75 metres, including 4.54% U3O8 and 3% nickel over 2.75 metres. ML-88 returned 0.66% U3O8 over 4.8 metres, including 1.58% U3O8 over 1.5 metres. Five days ago IUC announced additional drilling plans for Moore Lake, including areas previously untouched that are adjacent to McArthur mine.

Mongolian ExplorationIUC has an option to earn a 65% interest in Erdene Gold's (ERD) 32 uranium licenses in Mongolia. On top of that, it owns a 70% stake in the Gurvan-Saihan Joint Venture and is continuing to conduct exploration. Historical references suggest Gurvan-Saihan could contain 17.5 million lbs of uranium, but nothing has been proving with industry standards yet.

Fortress Minerals Corporation (FST) Ron Hochstein, the president of FMC is also the president of IUC. In 2004, FMC acquired some of IUC's mineral assets in Mongolia. IUC has about a 40% stake in FMC, valued at ~$40 million based on market capitalization.

Standard Uranium (URN)Recently, IUC announced that it has doubled its stake in Standard Uranium, owning 11.7% of the outstanding shares and using it as an investment vehicle. That's about a $3 million dollar investment.

ManagementChairman of Board of Directors: Lukas LundinLukas Lundin is the son of Adolf Lundin, as in Lundin Petroleum and Lundin Mining. Lukas is on the boards of many resource companies of various sizes; this list is extensive: Atacama Minerals, Canadian Gold Hunter, Canmex Minerals, Fortress Minerals, Lundin Mining, Newmex Minerals, Red Back Mining, Tanganyika Oil, Tenke Mining, TNR Gold, Valkyries Petroleum. He and his family have connections all over the place and represents a powerful force behind IUC.

President and CEO: Ronald HochsteinHochstein has been President of IUC since April 2000. He was previously a manager of Agra-Simons Mining Group operations in Toronto and before that, was with Noranda Inc. for 12 years. And according to SEDI, he has not sold a share of IUC in 11 months.

Mutual Fund BackingResolute Funds, including Resolute Growth and Resolute Performance, are two of the best performing Canadian funds (Resolute Growth gave a 130% return in the past year). Collectively, they own >10% of IUC.

When to Get In? Resolute Funds filed on February 8th to sell 184,100 shares and reduce its holding of IUC from 13.12 to 12.91% of all outstanding shares. This, along with the market correction, eroded IUC's share price as it fell to an intraday low of $5.50Cdn on February 14th, which approached its most recent low of $5.44Cdn on October 28, 2005.

The key for IUC in joining the ranks of promising producers like Urasia and Paladin will be an announcement to reopen their existing American mines. Although official word from the company is to wait until uranium prices head even further up before reopening, I am a little suspicious; it is unclear to me at this point whether they project that it is not cost-effective at current prices (something that I can't really believe), or that there are other hindrances in play (permits, Native American opposition).

It would be recommended at this point to wait until IUC announces reopening before buying this stock. Personally, I love the company, its potential, its assets, and the people behind it, but without certainty of impending and inevitable uranium production, IUC will always be worth less than half of Paladin or Urasia.

{kind=link}