IPO: Uranium Focused Energy Fund

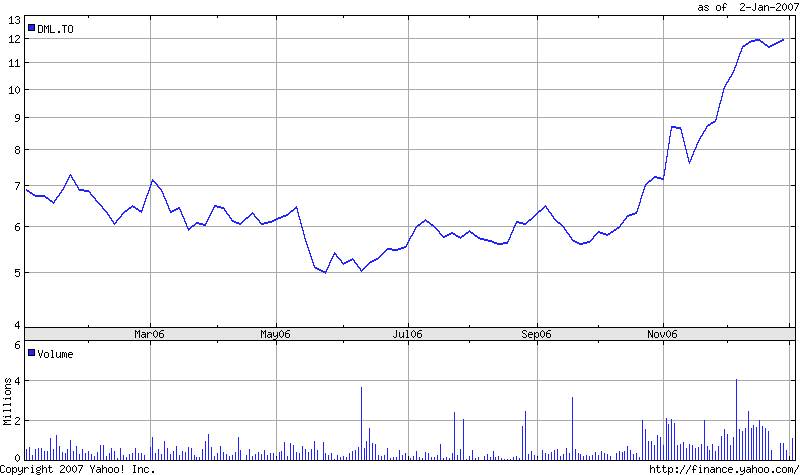

Just yesterday, Middlefield Group, with services in Canada through Middlefield Capital Corporation and managers of several mutual funds, announced that it was filing a preliminary prospectus in relation to the IPO of a new Uranium Focused Energy Fund. Middlefield already has several uranium stocks in its mutual funds, most notably the Middle Group Resource Class, which has Denison Mines (TSE:DML) 7.56% and SXR Uranium One (TSE:SXR) 6.44% as the two of the top three holdings; however, because that particular fund also has a lot of oil and natural gas exposure, its 1 year return of -7.85% was probably the impetus for starting a uranium-only mutual fund.

Let us parse through what Middlefield has to say about this new uranium fund..

In light of the significant capital and time requirements associated with the development of new uranium mines, the Advisor expects uranium prices to remain strong over the life of the Fund, which will terminate on December 31, 2013.

They clearly expect uranium supply-demand fundamentals to remain strong until 2013, which is a longer period of time than I would predict; it is widely acknowledged that the “easy money” has been made in uranium, but that there is upside for investors over the next 12-24 months.

the Portfolio will be focused on the securities of issuers that operate in or have exposure to the uranium sector, supplemented with the securities of other energy related issuers that operate in or have exposure to the energy sector. The Advisor expects that the weighting in uranium related securities will comprise approximately 75% of the value of the initial Portfolio and will include such companies as Cameco Corp., Paladin Resources Ltd., Denison Mines Corp. and sxr Uranium One Inc.

This may have an impact on the latter three companies, all of them near-term or already producing uranium. Depending on how enthusiastic investors are in this uranium fund, I expect these three companies to receive a further boost from institutional buying.

A uranium-only mutual fund is an interesting option; certainly, those investors who are looking for exposure to uranium but do not know what risk tolerance they are willing to take would be relieved to buy essentially a basket of uranium stocks.

Let us parse through what Middlefield has to say about this new uranium fund..

In light of the significant capital and time requirements associated with the development of new uranium mines, the Advisor expects uranium prices to remain strong over the life of the Fund, which will terminate on December 31, 2013.

They clearly expect uranium supply-demand fundamentals to remain strong until 2013, which is a longer period of time than I would predict; it is widely acknowledged that the “easy money” has been made in uranium, but that there is upside for investors over the next 12-24 months.

the Portfolio will be focused on the securities of issuers that operate in or have exposure to the uranium sector, supplemented with the securities of other energy related issuers that operate in or have exposure to the energy sector. The Advisor expects that the weighting in uranium related securities will comprise approximately 75% of the value of the initial Portfolio and will include such companies as Cameco Corp., Paladin Resources Ltd., Denison Mines Corp. and sxr Uranium One Inc.

This may have an impact on the latter three companies, all of them near-term or already producing uranium. Depending on how enthusiastic investors are in this uranium fund, I expect these three companies to receive a further boost from institutional buying.

A uranium-only mutual fund is an interesting option; certainly, those investors who are looking for exposure to uranium but do not know what risk tolerance they are willing to take would be relieved to buy essentially a basket of uranium stocks.

posted by Spelunca at 9:40 PM

1 comments

![]()

![]()